Cautious optimism as RBA pauses for second straight month

Sarah Dowling, Property News Editor

First published 01 August 2023, 02:37 PM

Last updated 01 August 2023, 02:50 PM

At its August board meeting on Tuesday the RBA kept the official cash rate at 4.1% - where it's remained since June - as inflation continues to track lower and household spending slows.

"The higher interest rates are working to establish a more sustainable balance between supply and demand in the economy and will continue to do so," RBA governor Philip Lowe said in a post-meeting statement, the second last before his term ends in mid-September

"In light of this and the uncertainty surrounding the economic outlook, the board again decided to hold interest rates steady this month. This will provide further time to assess the impact of the increase in interest rates to date and the economic outlook."

Since reaching a peak of 7.8% in the December 2022 quarter, the annual rate of inflation has been cooling faster than expected with the latest Consumer Price Index easing to 6% in the June 2023 quarter, down from 7% in March.

While that’s still well above the RBA’s 2-3% inflation target, updated forecasts released Tuesday predict CPI will ease to around 3.25% per cent by the end of 2024 and to be back within the target range in late 2025.

The RBA has held interest rates at 4.1% since June. Picture: Getty

PropTrack senior economist Eleanor Creagh says that takes some pressure off the RBA, allowing more time to assess the outlook as it tries to engineer a soft landing whilst returning inflation to target.

“Though still high relative to history and well above the RBA’s 2-3% target range, CPI inflation was below both market expectations and the RBA’s official forecasts and looks set to continue to moderate and move lower into the first half of 2024,” Ms Creagh said.

“Despite the tight labour market, with the unemployment rate holding at a multi-decade low of 3.5%, and still rising services inflation, the full impact of recent rate rises is yet to be felt and we’re likely to continue to see inflation moving lower.”

But the RBA still hasn’t closed the door to future rate hikes if inflation takes too long to return to target, saying the priority is to return inflation to target within a reasonable timeframe.

"The recent data are consistent with inflation returning to the 2–3% target range over the forecast horizon and with output and employment continuing to grow. There are though significant uncertainties." Mr Lowe said

Home prices now higher than a year ago

With interest rates now widely tipped to have peaked, Ms Creagh says confidence is returning to the property market - setting the stage for a strong spring selling season.

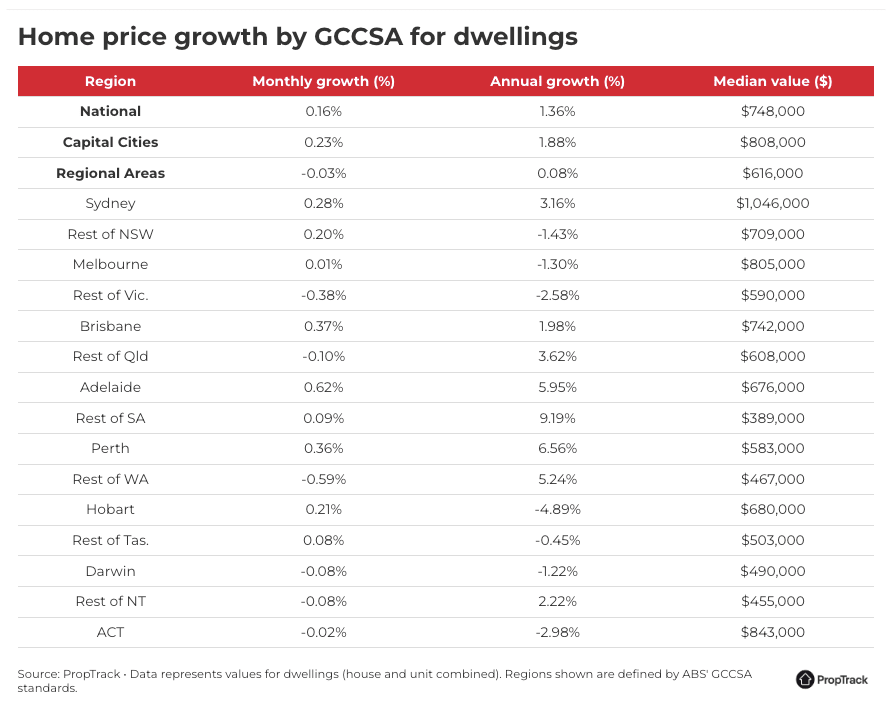

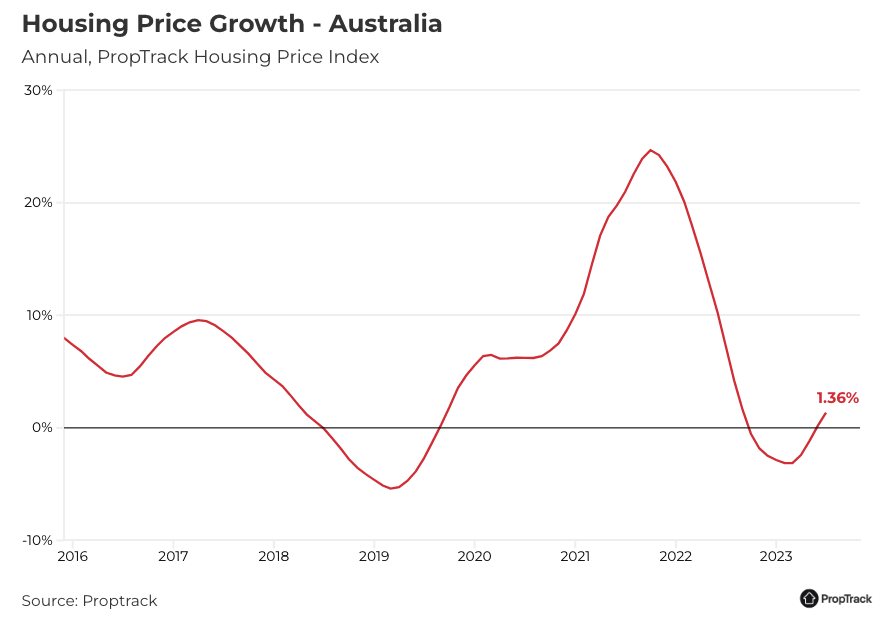

The latest PropTrack Home Price Index rose for a seventh consecutive month in July, reversing much of the falls recorded over 2022, and taking national home prices 1.36% higher than a year ago.

During the month, the value of an average Australian home lifted by 0.16% to a median $748,000.

Ms Creagh says home prices are now just 1.44% below the March 2022 peak nationally, with some capital cities reaching new record highs.

“Stronger housing demand and a limited flow of new listings hitting the market have offset the impact of substantial interest rate rises that have been pushed through since May 2022,” she said.

“Although total stock on market has increased slightly, the flow of new listings has remained soft in recent months, leading to increased buyer competition and solid selling conditions with prices continuing to lift.”

All capital cities except Darwin and Canberra saw prices rise in July, led by Adelaide where prices grew 0.62% to an all-time high of $676,000. Brisbane and Perth also set new peaks with prices up 0.37% and 0.36% respectively.

Sydney prices recovered a further 0.28% to a median of $1,046,000, sitting just 2.22% below the February 2022 peak, while Melbourne inched up 0.01% to a median $805,000.

“Melbourne's recovery has not been nearly as sharp as Sydney, though it did not see as large a decline in 2022,” Ms Creagh said.

“As a result, prices in Melbourne are still 4.91% lower than the March 2022 peak and 1.3% lower than a year ago.”

Property prices have risen for seven consecutive months as demand outstrips supply. Picture: Getty

Hobart prices rose 0.21% to $680,000 in July but remain down 6.6% from the March 2022 peak.

“However, this comes after several years of outperformance as well as strong growth during the pandemic. Home prices in Hobart are still up 38.3% since March 2020,” Ms Creagh said.

Strong lead in to the spring selling season

While winter is traditionally a quiet period for the property market, limited stock and unseasonably high buyer demand in some cities and regions is putting sellers in a prime position ahead of spring.

“Given limited new stock is coming to market, buyer interest is being concentrated, leading to increased competition and solid selling conditions that are seeing prices continue to lift,” Ms Creagh said.

“Seven months of price rises that have gathered traction across markets could also be drawing buyers off the sidelines.”

She says while the full impact of recent rate rises is yet to be felt, broader market activity suggests confidence is returning.

“Sales volumes have increased, auction activity has strengthened, and auction clearance rates are holding firm,” Ms Creagh said.

“Many buyers and sellers anchor expectations from recent momentum, which can embed trends in market, with buyers likely comforted by greater certainty around economic activity, continued low unemployment and talk of the interest rate rise cycle reaching a peak.

“This is likely to sustain confidence and maintain the lift in home prices into spring, resulting in more markets returning to positive annual price growth.”

Have interest rates peaked?

There’s cautious optimism that we may have reached the peak of the interest rate cycle, with the RBA holding interest rates at 4.1% since June 2023 - the longest pause since it began raising the cash rate in May 2022.

While financial markets expect the cash rate has peaked, economists are divided over whether one more increase is needed.

ANZ is forecasting an ‘extended pause’ at 4.1% until late 2024, when it says the RBA will start to cut interest rates.

Economists at Westpac and CBA had anticipated one final rate hike in August, to take the cash rate to a peak of 4.35%.

NAB has not ruled out one or two more rate hikes, but expects sharp falls from mid-next year will take the cash rate to 3.1% by December 2024.

Modelling from realestate.com.au shows a reduction in the cash rate from 4.1% to 3.1% would free up around $327 a month for a borrower with $500,000 outstanding on their mortgage, assuming their lender passes any cuts on in full.

Increase to monthly repayments since May 22:

| Loan size | 4.1% cash rate | 3.1% cash rate | Difference |

| $500,000 | $1,209 | $882 | $327 |

| $750,000 | $1,814 | $1,323 | $490 |

| $1,000,000 | $2,418 | $1,765 | $653 |

In these calculations, the borrower is assumed to be an owner-occupier paying principal and interest with 30 years remaining on their loan. It assumes an initial average variable interest rate of 2.86%, according to April 2022 RBA figures. The calculation does not factor in loan fees and charges, or any principal paid down over time.

Mortgage Choice CEO Anthony Waldron says while the latest pause will be welcome news for borrowers, that didn’t stop the nation’s lenders from lifting rates on some fixed- and variable-rate home loan products last month.

“It’s not yet clear if the Reserve Bank will keep the cash rate on hold for an extended period, but with rates already having increased so rapidly since May last year, borrowers with fixed rates ending soon and those looking for a better deal should speak to a mortgage broker to understand their options," Mr Waldron said.

Originally published at: https://www.realestate.com.au/news/cautious-optimism-as-rba-pauses-for-second-straight-month/